|

ITALY

POPULATION:

60,8 MLN

SOURCE:

UNIONE

NAZIONALE RAPPRESENTANTI AUTOVEICOLI ESTERI

(UNRAE.IT) |

|

Immatricolazioni Fiat, Lancia-Chrysler, Alfa Romeo, Jeep

in ITALIA

|

|

Registrations Fiat,

Lancia-Chrysler, Alfa Romeo, Jeep in

ITALY

|

|

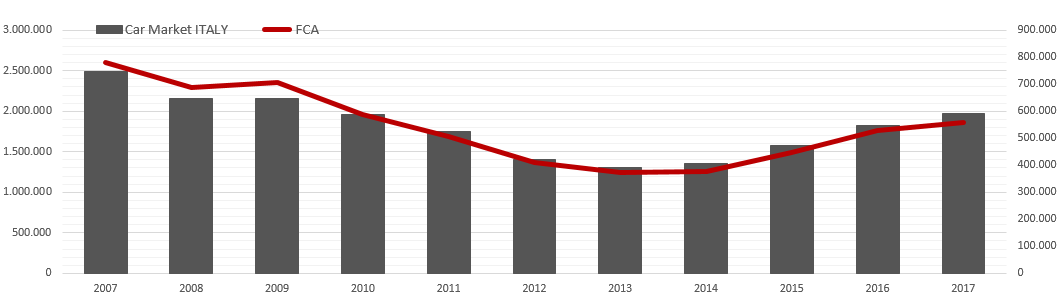

Il

mercato auto in Italia ha confermato nel 2017 il buon progresso

dell'anno precedente e con 1.970.497 immatricolazioni è cresciuto del

7,9% sul 2016, restando però ancora ben lontano dalle vendite registrate

nel 2007.

Il Gruppo Fiat Chrysler Automobiles,

leader in Italia, ha fatto molto bene con i marchi Alfa Romeo trainata

dal suv Stelvio (+24,6%) e Jeep in rialzo del 22,3% sul 2016 grazie alla

buona accoglienza per la Compass.

Volkswagen, Ford e Renault guidano i competitors guadagnando

immatricolazioni rispetto al 2016, così come Peugeot, Opel, Toyota,

Citroen, Audi, Mercedes e Nissan.

La Fiat

Panda è stato il modello più venduto nel 2017 in Italia, con più del

doppio delle vendite rispetto agli altri modelli del Gruppo FCA, tra i

quali spiccano i risultati della Lancia Ypsilon (al secondo posto), Fiat

Tipo e Fiat 500. Interessante il debutto dell'Alfa Romeo Stelvio e della

Jeep Compass. |

|

The car market in Italy in 2017 confirmed

the good progress of the previous year and with 1,970,497 registrations

grew by 7.9% on 2016, but remains still far from the sales recorded in

2007.

The Fiat Chrysler Automobiles Group,

leader in Italy, did very well with the brands Alfa Romeo driven by the

SUV Stelvio (+24.6%) and Jeep up by 22.3% on 2016 thanks to the good

reception for the Compass.

Volkswagen, Ford and Renault lead the

competitors gaining registrations previous year, as did

Peugeot, Opel, Toyota, Citroen, Audi, Mercedes and Nissan.

The Fiat Panda was the best selling model

in 2017 in Italy, with more than double sales compared to other models

of the FCA Group, among which are the results of the Lancia Ypsilon (in

second place), Fiat Tipo and Fiat 500. Interestingly the debut of the

Alfa Romeo Stelvio and Jeep Compass. |